Is a 2nd Pillar Buyback/Voluntary Purchase Worth It?

You could be better off by CHF 20-40,000 by not adding to your 2nd pillar

It’s coming to the end of the year. Soon there will be Christmas songs on the radio, the snow will come, and with it – hopefully – a well-earned break with loved ones following a productive year.

In Switzerland, that also means it’s coming to the end of the tax year.

Is a 2nd pillar buyback/voluntary contribution/top up worth it?

The answer depends on your income level, family situation, cantonal and local tax residency, and risk appetite.

Hold on – risk appetite? Yes, risk appetite.

That’s because one of the biggest considerations for a 2nd pillar contribution is not the tax deduction – it is the opportunity cost.

Investopedia defines opportunity cost as ‘… the potential forgone profit from a missed opportunity—the result of choosing one alternative over another’.

If you did not put that money into your 2nd pillar pension, where else could you invest your money? What better (or worse) returns could you get? How much more flexible would the access to your money be? Could you still benefit from a tax saving later?

Accountants always recommend extra 2nd pillar purchases for the tax deductions. But what about the loss in growth, flexibility and early retirement?

Case study 1 - Zurich

Sam is 40 years old, married, has 2 children, and is living in 8003 Zurich.

Gross annual income is CHF 200,000.

2nd Pillar buyback:

- CHF 10,000 voluntary purchase to the 2nd pillar

- = CHF 3,262 tax savings

- CHF 10,000 x 1% growth (1% based on 2nd pillar mandatory, the over-mandatory typically grows at 0.25%)

- = CHF 12,202 + CHF 3,262 = CHF 15,464 TOTAL at age 60 (CHF 5,464 profit)

- = CHF 12,824 + CHF 3,262 = CHF 16,086 TOTAL at age 65 (CHF 6,086 profit)

Vs.

Investment:

- CHF 10,000 investment into an investment account or flexible pension (pillar 3b)

- No tax deduction (but grows & distributes tax free in the case of pillar 3b)

- CHF 10,000 x 5.5% growth (based on the average pillar 3b)

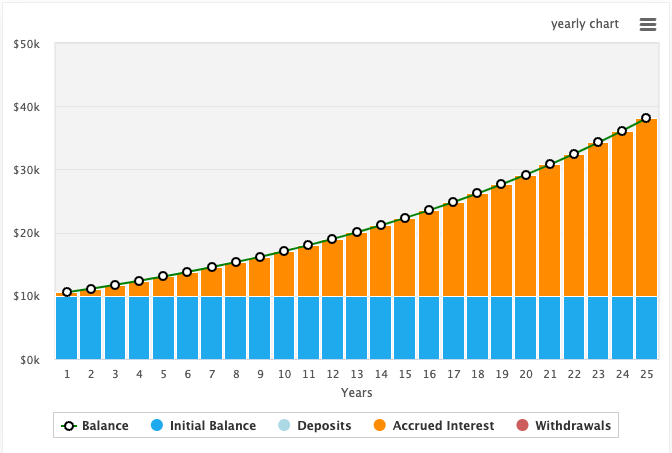

- = CHF 29,178 at age 60

- = CHF 38,134 at age 65

Result

- Pillar 3b = + CHF 23,714 extra by age 60

- Pillar 3b = + CHF 32,048 extra by age 65

Extra Tax Optimisation

Using a pillar 3b from age 43 to 59 (instead of age 60), Sam can;

- Grow CHF 10,000 to CHF 27,656 (5.5% x 19 years)

- Use the profits to make a 2nd pillar buyback of CHF 27,656 at age 59

- Get a 2nd pillar tax deduction of CHF 8,521 based on an income of CHF 200,000

- Likely get a higher tax deduction, since Sam's salary will likely be higher than today

Case study 2 - Geneva:

George is 40 years old, married, has 2 children, and is living in 1202 Geneva.

Gross annual income is CHF 200,000.

2nd Pillar buyback:

- CHF 10,000 voluntary purchase to the 2nd pillar

- = CHF 3,945 tax savings

- CHF 10,000 x 1% growth (1% based on 2nd pillar mandatory, the over-mandatory typically grows at 0.25%)

- = CHF 12,202 + CHF 3,945 = CHF 16,147 TOTAL at age 60 (CHF 6,147 profit)

- = CHF 12,824 + CHF 3,945 = CHF 16,769 TOTAL at age 65 (CHF 6,769 profit)

Vs.

Investment

- CHF 10,000 investment into an investment account or flexible pension (pillar 3b)

- = CHF 2,044 tax saving (CHF 5,174 deduction: CHF 3,348 couple + CHF 913 x 2 children)

- CHF 10,000 x 5.5% growth (based on the average pillar 3b)

- = CHF 29,178 + CHF 2,044 = CHF 31,222 at age 60

- = CHF 38,134 + CHF 2,044 = CHF 40,178 at age 65

Result

- Pillar 3b = + CHF 25,075 extra by age 60

- Pillar 3b = + CHF 33,409 extra by age 65

Additional Considerations

- The pillar 3b and investment accounts are typically flexible to access before retirement, without having to leave Switzerland, retire, or use towards a property or company (like the 2nd pillar or pillar 3a)

- 2nd pillar and 3rd pillar (pillar 3a and 3b) can be pledged (Verpfändung) towards a Swiss property purchase or property repayment

- Contributions to the pillar 3b and investment accounts are without a maximum annual limit

- Contributions to pillar 3b are non-tax deductible (except for Geneva and Fribourg)

- Contributions to pillar 3b in Geneva are tax deductible to (2022):

- CHF 2,232 per person

- CHF 3,348 per couple

- CHF 913 per child

- Higher annual yields compound to produce higher total returns

- Pillar 3b projections based on CHF 10,000 over 20 years result in the following:

- CHF 20,938 at 3%

- CHF 68,485 at 8%

- CHF 108,347 at 10%

If you are interested in optimising your finances - saving more and paying less tax - you can read contact us here.

If you would like to know how much you will have, or how much you will need, to retire – use our free retirement calculator here.

Disclosure:

This article has not been written to give advice, and purely expresses our own opinions. We are not receiving any compensation for it, and we are not responsible or liable in our capacity as an independent financial adviser for any action taken by readers based on these opinions. For personalised advice based on these issues, please seek advice from a regulated, independent expert.