When geopolitical risk erupts into open conflict, markets reprice fast. For globally mobile investors, particularly English-speaking expats with cross-border assets and liabilities, the key question is not simply what is happening between Iran, Israel, and the USA, — but how war reshapes capital flows, interest rates, currencies, and long-term investments.

The invasion of Ukraine in 2022 offered a live stress test of modern markets under military shock. From oil and gold to Bitcoin, defence stocks and the Swiss franc, we witnessed how assets behave when uncertainty spikes. As tensions escalate in the Middle East after the United States and Israel launched coordinated strikes against Iran on 28th February 2026, investors would be wise to revisit those lessons.

How Markets Reacted to the Russia/Ukraine Invasion

When Russia invaded Ukraine in February 2022, markets moved in predictable but nuanced ways.

Gold surged almost immediately. As a traditional safe haven, gold climbed sharply in the weeks following the invasion, briefly approaching record highs. Investors sought protection from geopolitical uncertainty, sanctions risk, and potential inflation shocks driven by disrupted commodities.

Oil prices spiked even more dramatically. Brent crude surged above $120 per barrel as markets priced in supply disruptions from one of the world’s largest energy exporters. Russia’s role in global energy, combined with sanctions and self-sanctioning by buyers, created a rapid repricing in global energy markets.

Bitcoin’s reaction was more complex. Initially, Bitcoin fell alongside risk assets, reflecting its status at the time as a volatile, liquidity-sensitive asset. However, it later recovered as narratives emerged around censorship resistance and financial sovereignty. The conflict demonstrated that Bitcoin can behave both as a speculative risk asset and, in certain contexts, as a geopolitical hedge — though not yet a consistent safe haven like gold.

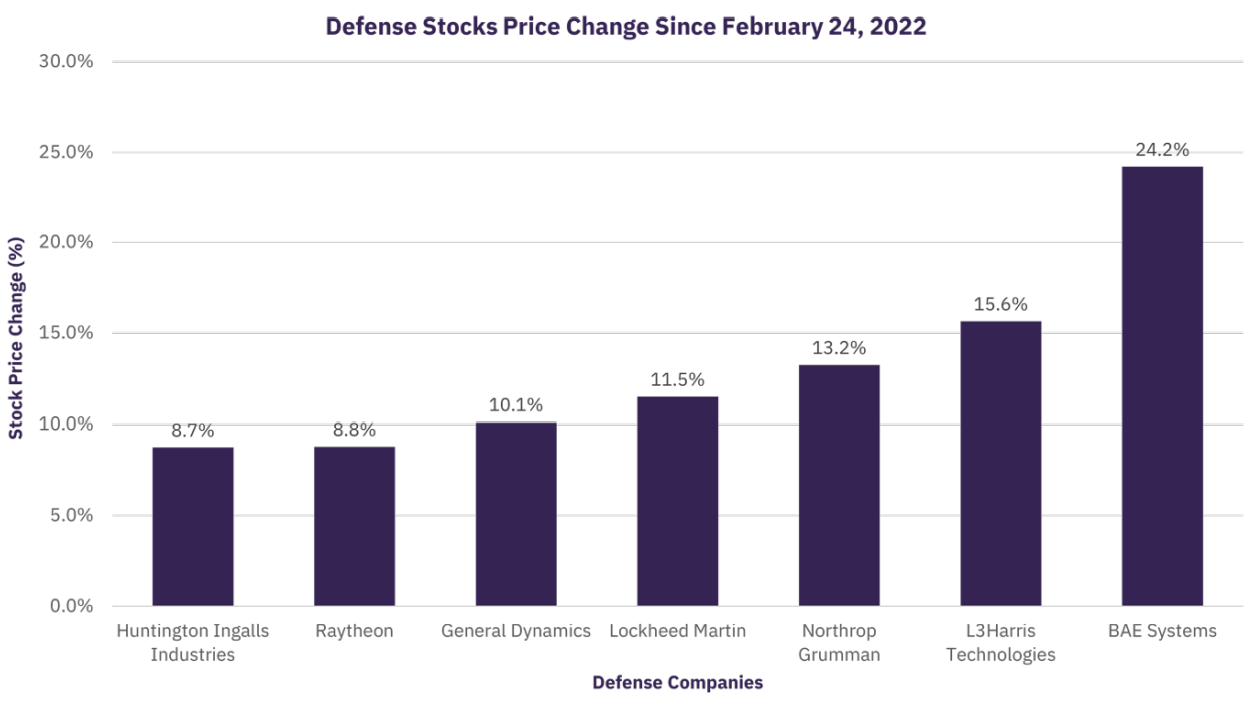

Defence stocks were clear beneficiaries.

European and US defence contractors rallied strongly as governments announced sharp increases in military spending. Germany’s historic rearmament pledge marked a structural shift. The lesson was clear: modern conflicts trigger sustained fiscal commitments, not just temporary spending spikes.

Meanwhile, the Swiss franc strengthened. As geopolitical risk increased, capital flowed toward perceived stability. Switzerland’s political neutrality, strong balance sheet and credible monetary policy reinforced the franc’s reputation as a defensive currency.

What Could Happen Now in the Iran War?

In this current Middle East war, we could see a similar pattern with different mechanics, but similar transmission channels, play out.

The most immediate impact will likely be in oil markets. Unlike Russia, Iran’s strategic leverage is less about export volume and more about geography. The Strait of Hormuz remains one of the most critical chokepoints in global energy supply. As of today, that passage has been ‘closed’ by Iran’s Revolutionary Guard. Whether that will be enforceable remains to be seen, however, any threat to shipping routes could produce sharp oil price spikes, even without sustained production losses.

Higher oil feeds directly into inflation expectations. That, in turn, influences interest rates. But here is where the analysis becomes more nuanced.

During the Ukraine war, inflation was already elevated. Energy shocks compounded an existing problem. In the Iran conflict, central banks may need to balance two competing forces: inflationary oil spikes versus potential growth slowdowns from geopolitical instability.

For expat investors, this matters enormously. If growth deteriorates while energy prices rise, we could see a stagflationary dynamic. In that environment, central banks may hesitate to tighten aggressively. In fact, over time, governments historically finance wars through higher deficits, which often lead to looser monetary conditions or financial repression.

Wars are expensive. They are rarely paid for through immediate taxation. Instead, they are funded via borrowing. If borrowing expands materially, bond supply rises. Central banks may face pressure – explicit or implicit – to maintain accommodative policies to keep debt service manageable. That could mean structurally lower real interest rates over time.

Oil, Gold and the Return of the Safe Haven Trade

It is still early days in this conflict; however, it is likely that oil becomes the first transmission channel, with gold likely reasserting its role as a safe haven.

Gold’s appeal strengthens when three conditions align: geopolitical risk, fiscal expansion, and concerns about fiat currency debasement. The conflict with Iran and regional powers — particularly if it threatens energy infrastructure — checks at least two of those boxes.

The Swiss franc may also strengthen once more. CHF has historically benefited during periods of geopolitical stress. For expats holding multi-currency portfolios, Swiss exposure can act as a volatility dampener when emerging market or commodity-linked currencies experience turbulence.

Bitcoin’s role remains less predictable. If capital controls expand, sanctions intensify, or digital payment systems become politicised, crypto assets could benefit at the margin. However, in liquidity-driven selloffs, Bitcoin may still trade as a risk asset before stabilising.

Energy, Commodities and the AI Investment Supercycle

There is another layer to this discussion that did not exist in the same way during the early stages of the Ukraine conflict: the acceleration of AI infrastructure investment.

Artificial intelligence data centres require enormous amounts of electricity. The build-out of computing infrastructure is driving structural demand for power generation, grid upgrades, transmission lines and backup capacity. That means rising demand for copper, aluminium, steel and specialist materials.

Copper, in particular, is central to both the energy transition and AI expansion. It is used in grid infrastructure, electric vehicles, renewable installations and data centre construction. If geopolitical conflict disrupts global trade flows while AI investment continues, supply constraints could collide with structurally rising demand.

Energy markets are therefore facing a dual pressure: geopolitical risk on supply, and technological transformation on demand.

If oil spikes due to the Iran conflict while electricity demand rises due to AI expansion, capital expenditure in energy infrastructure could accelerate. That benefits not only oil producers, but also energy services, grid developers and materials companies.

Unlike nuclear weapons, nuclear energy is increasingly recognised – even by some policymakers – as one of the few scalable sources capable of satisfying the world’s rising energy requirements while maintaining low carbon emissions.

The Ukraine crisis accelerated focus on energy independence and diversification away from fossil fuels and now, in the context of AI’s power demands, nuclear energy capacity is being reassessed as a core element of future grids. Sectors exposed to nuclear energy infrastructure – including utilities, engineering firms, and materials suppliers – could see elevated investor interest as governments prioritise resilient, low-carbon energy supply.

Monetary Policy: How Will War Be Paid For?

The Ukraine conflict reinforced a key truth: fiscal dominance can re-emerge quickly.

European governments expanded defence budgets. The United States approved large-scale aid packages. Budget deficits widened. Debt issuance increased.

If the Iran war becomes protracted, similar patterns are likely. The political appetite to fund military and strategic spending tends to be high during security crises. Over time, this can alter monetary policy trajectories.

Whilst initial inflation spikes from oil could delay rate cuts, medium-term dynamics may favour looser policy if growth slows and debt burdens rise. Central banks may find themselves balancing price stability against financial stability and sovereign funding costs.

For expat investors with broad exposures, this raises strategic questions about duration exposure, inflation hedges, currency allocation and real assets. Gold, energy producers, materials and selected infrastructure assets may serve as partial hedges in a world where fiscal expansion becomes persistent.

The Bigger Picture for International Investors

The lesson from the Russia/Ukraine war was not simply that oil goes up and gold rallies. It was that geopolitical shocks can accelerate existing structural trends.

In 2022, energy security became a policy priority overnight. Defence spending reset higher. Inflation dynamics shifted. Today, we are simultaneously navigating geopolitical fragmentation, AI-driven electricity demand, commodity constraints and evolving monetary policy.

The Iran/Israel/US war adds additional layers of complexity onto an already fragile global system.

For internationally diversified investors, the key is not prediction, but preparation. Holding a portfolio that recognises the role of safe haven assets, understands the sensitivity of oil and commodities, and accounts for the long-term implications of fiscal expansion and shifting interest rates is increasingly important.

Geopolitics cannot be timed. But it can be managed.

In uncertain times, disciplined allocation across real assets, defensive currencies like CHF, selective growth themes such as AI, and quality global equities can help ensure portfolios are positioned not just to withstand volatility — but to adapt to it.

History does not repeat exactly, but it often rhymes. The investors who navigate the next phase of global conflict most effectively will be those who have already absorbed the lessons of the last one.